The Stolen Trusteeship: How Mr Durrant’s Fund Manager Became an Impostor Trustee After His Murder.

- jordandurante81

- Dec 19, 2025

- 11 min read

“The concealment of a financially motivated murder: the killing of an RAF Squadron Leader for his offshore assets.”

While Mr Durrant was alive, he used [XXXXXXX] Trust Company as his fund managers, in the same manner that Mr Robert Maxwell did during his lifetime. They were not trustees.

Following Mr Durrant’s financially motivated murder, these fund managers unilaterally appointed themselves as trustees of Mr Durrant’s assets and companies. They purported to do so by relying on a so-called trust deed that does not contain Mr Durrant’s name, the name of any family member, nor Mr Durrant’s signature but names the Freemasons as the beneficiaries. In substance and in law, this renders the document worthless.

Crucially, this self-appointed “trustee” never produced the alleged deed to the Royal Trust Bank in the Isle of Man, where an account existed in the name of the Emerald Trust. Any legitimate trustee would have known of this account and would have been able to access it. Their inability to do so is fatal to their claim of trusteeship which will be shown in a new file soon.

The documents set out below demonstrate beyond any doubt that the true trustees were not this Jersey trust service provider, and that the trusteeship was wrongfully seized after Mr Durrant’s brutal murder.

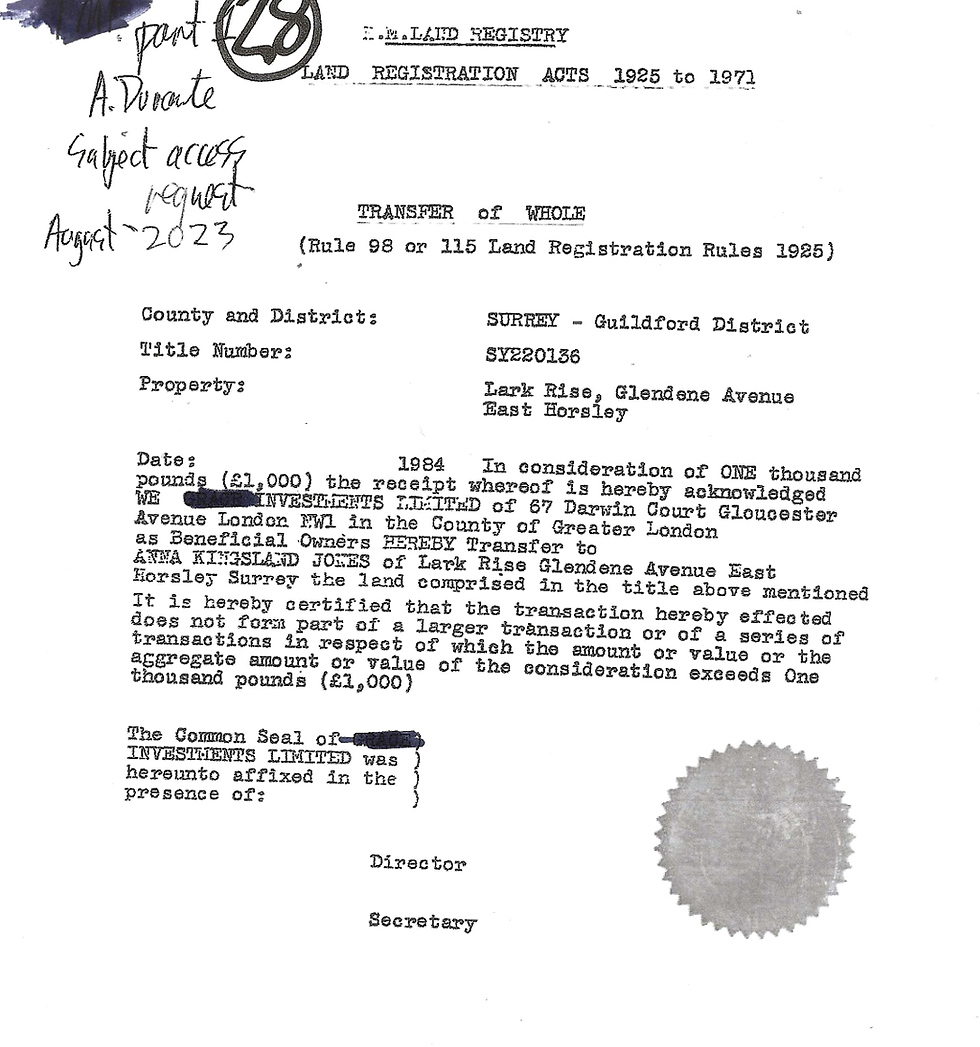

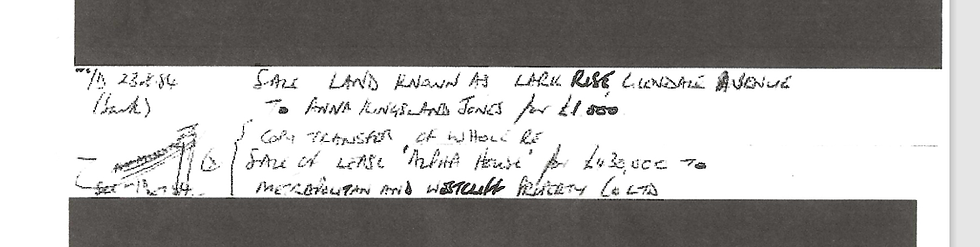

Set out below is a Land Registry document relating to a property known as Lark Rise. This document clearly records Anna Kingsland-Jones as the trustee. Anna Kingsland-Jones is Jordan’s mother and the daughter-in-law of Mr James William Durrant.

The document is significant because it confirms Anna Kingsland-Jones’s role as a trustee for Mr Durrant, establishing a continuous timeline of her involvement from the 1970s and continuing after Mr Durrant’s financially motivated murder. This directly contradicts the narrative later advanced by trust service providers and lawyers who sought to erase or ignore her trusteeship.

Jordan has now followed the money. The next step is to follow the properties. By doing so, the public will be able to see the truth about who the two trustees chosen by the settlor actually were, and how those lawful trustees were deliberately disregarded.

Despite this documentary evidence, lawyers and courts have repeatedly ignored these facts and instead sought to silence Jordan, prioritising the protection of institutional and international reputations over justice. That is a position Jordan does not accept — and will not accept — at any cost.

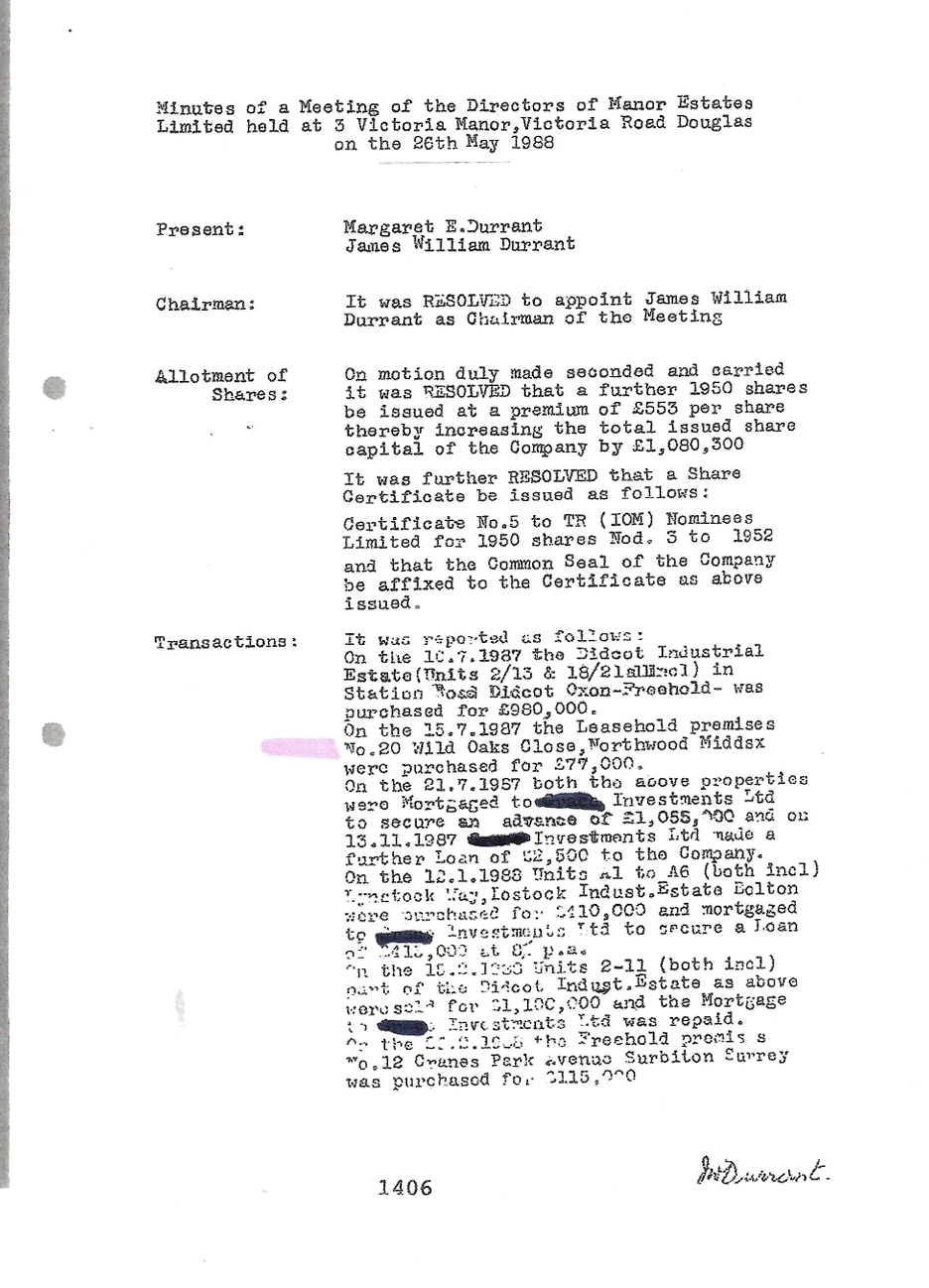

The meeting notes set out below relate to the Isle of Sark and indicate the involvement of individuals known to Mr James William Durrant, including Commander Hudson of the British Navy. Mr Durrant would have known Commander Hudson during the Second World War, or at the very least would have been aware of each other’s wartime activities. Their later connections through the offshore islands and their involvement in the so-called trust service providing industry strongly suggest a continuity of association beyond the war years.

Of particular significance is the fact that Mr George Stuart, the fellow trustee of Mr Smalley, entered into business with Commander Hudson after Mr Durrant’s murder. Mr Stuart was also in business with the convicted fraudster Mr Costain, who in turn is connected to Robert Maxwell’s companies.

These overlapping relationships, emerging after Mr Durrant’s death, raise serious questions about coordination, continuity, and the post-murder control of assets and trusteeship.

These notes also reference Anna Kingsland-Jones and the Lark Rise property, further corroborating Anna Kingsland-Jones’s long-standing involvement and role in matters connected to Mr Durrant and his affairs.

Taken together, these records reinforce the established timeline of relationships, trusteeship, and property interests that existed well before and after Mr Durrant’s murder, and which have since been repeatedly ignored or obscured.

The document below is a letter written by Mr James William Durrant to his fund managers, expressly referring to the Lark Rise property. This correspondence further evidences Mr Durrant’s direct involvement in, and control over, matters relating to the property during his lifetime.

Set out below is an extract from the Subject Access Request (SAR) disclosure provided by the impostor trustee, which records the Lark Rise property and identifies Anna Kingsland-Jones in connection with it.

It is important to note at this stage that the impostor trustee has refused to comply with Subject Access Requests (SARs) submitted by both Jordan and his father, the direct beneficiary of the Emerald Trust. In rejecting those requests, the impostor trustee labelled both individuals as “financially motivated”, a position that was subsequently endorsed by the Jersey Commissioner.

This stance closely mirrors the approach taken in the Abramovich case in Jersey, where access to personal data and transparency were likewise restricted on highly questionable grounds.

Notwithstanding this, even if relevant emails or records have since been deleted, Jersey has now committed to mandatory electronic and crypto-related data retention regimes. Accordingly, should the courts choose to act lawfully and in the interests of justice, these communications ought to remain recoverable through proper disclosure procedures and forensic examination.

The meeting notes from Sark once again record Anna Kingsland-Jones and the Lark Rise property. Significantly, the individuals named in these notes are those who later became the impostor trustee after Mr Durrant’s murder.

At the time of these meetings, however, their conduct is consistent not with that of a trustee, but rather with that of a fund manager, reinforcing the position that no legitimate trusteeship existed prior to Mr Durrant’s death and that the role was assumed only afterwards.

The Land Registry document set out below shows that Manor Estates (Isle of Man) acquired the property 20, Wild Oaks, which was previously held by Anna Kingsland-Jones as trustee.

This raises a critical question. When Mr Smalley took control of Manor Estates in 1990, why did he never disclose that Anna Kingsland-Jones was the trustee of the property? Why was this fact concealed from the rightful trustee and from the Durante family for decades, only coming to light through my own research?

As the reader will shortly see, Mr Smalley was fully aware of Anna Kingsland-Jones’s trusteeship and even referred to it in meetings with the impostor trustee. Yet he never raised this issue with the Durante family, nor did he take any steps to use this information to recover the Emerald Trust and its assets from the impostor trustee ever.

The answer appears self-evident. Mr Smalley and the impostor trustee have been working together for decades. This is further evidenced by the fact that the impostor trustee was also an impostor shareholder in Manor Estates. In 2017, the impostor trustee returned those shares to Mr Smalley, expressly stating that they held no declaration of trust entitling them to hold the shares.

That admission alone confirms my allegation: that the impostor trustee acted as an unauthorised and illegitimate shareholder for decades following Mr Durrant’s murder, mirroring their conduct as an impostor trustee.

More information below on the property 20,Wild Oaks.

Set out below is a letter from the impostor trustee to my father’s UK solicitor at the time, together with a document taken from their own archives, which they sought to rely upon to mislead the lawyers then acting. That strategy was effective at the time, but only because the wider documentary record was never properly examined. Decades later, after I became directly involved in the case, I reviewed every letter in detail and reconstructed the full chronology.

The archived letter relied upon is a letter written by Mr James William Durrant himself, dated 18 July 1987. In that letter, Mr Durrant refers to the fact that “the trustee has executed the trust document” in relation to the property 20, Wild Oaks.

When this statement is read alongside the trust deed produced later, its true significance becomes clear. The deed shows that Anna Kingsland-Jones was the trustee. Mr Durrant would not have written to a trustee stating that the trustee had executed the deed if the recipient themselves were the trustee. The language used is decisive.

This correspondence therefore provides further confirmation that the parties who later appointed themselves as trustees were not acting as trustees during Mr Durrant’s lifetime, but rather as fund managers. Their claim to trusteeship only arose after Mr Durrant’s financially motivated murder, reinforcing the conclusion that the trusteeship was self-appointed and illegitimate.

Set out below is the trust deed located by Jordan, to which Mr James William Durrant was referring in his letter above. Crucially, this deed does not name the impostor trustee as trustee. Instead, it names the company solely in its capacity as a company, not as a trustee.

This distinction is critical. It confirms that the entity later claiming to be trustee was not appointed as such under this deed, and further supports the conclusion that its subsequent claim to trusteeship arose only after Mr Durrant’s death, without lawful foundation.

Set out below is a letter from my father’s UK solicitor at the time, in which he records a meeting with a director of the impostor trustee. The solicitor’s notes from that meeting explicitly record Anna Kingsland-Jones as holding property on trust, and they also refer to Mr James William Durrant’s expressed wishes.

Those wishes were never followed.

Both of Jordan’s uncles subsequently died without ever receiving any benefit from the Emerald Trust, and for decades the trust produced no accounts and made no distributions to the Durante family. In reality, the Emerald Trust functioned as a trust in name only.

Remarkably, the first ever payment and the first meaningful accounting provided to the Durante family occurred only after Jordan presented his research to the organisation acting as trustee. That research set out, in detail, the organisation’s connections to Robert Maxwell, alongside other serious matters, including historic links to drug trafficking and arms dealing networks that Jordan was actively investigating.

Shortly thereafter, a payment was suddenly made.

The question therefore answers itself: what is the purpose of a trust that never accounts and never pays its beneficiaries?

The notes set out below show that the property 20, Wild Oaks is expressly mentioned. They also record that the other trustee, Mr Vaart, was identified by my father at the time. My father was, however, operating in an extremely difficult position. The contents of Mr Durrant’s safe were never released to the family, meaning that when an entity impersonates a trustee, there is very little documentary material to rely upon. Despite this, my father clearly knew Mr Vaart’s name and understood something of his true legal status as trustee, a fact demonstrated in the document shown immediately prior to this one.

The documents that appear partially blanked out by computer redaction originate from the impostor trustee. They were disclosed only because the impostor trustee could not lawfully refuse my mother’s Subject Access Request, once I demonstrated that my mother was in fact the trustee, not them. Notably, they continue to refuse to address this central point, despite the volume of documentary evidence and research now presented.

That refusal to engage is precisely why this material is now being taken public. If the impostor trustee continues to avoid a proper meeting and lawful scrutiny, these disclosures will proceed in full and transparently, so that the public can see exactly how this trusteeship was misrepresented and concealed for decades.

ghjkj

The letter set out below is from Jordan’s father’s UK solicitor and is headed “Jersey Trusts”. In due course, this section will expand to address the other trusts that were taken or diverted following Mr James William Durrant’s murder. It is sufficient to say at this stage that Jordan has now identified these trusts, and holds the relevant deeds, none of which name the Freemasons as beneficiaries of Mr Durrant’s wealth.

A number of trusts remain unaccounted for, and they consistently lead back to the same impostor trustee. Of particular significance is the trust deed dated 9 January 1969, which leads directly to Guernsey and forms a key part of the wider picture.

The letter also records a notable point: it refers to what is described as a “bold venture” by the Inland Revenue, following correspondence sent to Anna Kingsland-Jones in relation to a substantial tax liability running into millions.

This raises an obvious and important question. Why was the Inland Revenue writing to Anna Kingsland-Jones in relation to these companies at all? What did the Revenue understand about her true legal status, and what information were they relying upon when addressing her directly?

That question goes to the heart of who was recognised, in practice, as holding control and responsibility at the time — and who was not.

Set out below are internal notes from the impostor trustee’s solicitors, a law firm that represented “John” for decades and has also acted for the impostor trustee since 1989. This is the same firm whose conduct Jordan is now challenging, and whose activities and client relationships over several decades will be examined in detail in forthcoming disclosures.

A review of these notes is deeply revealing. They show that the impostor trustee kept no trustee minutes, produced no proper accounts, and failed to operate any of the basic governance mechanisms expected of a lawful trustee. Most strikingly, a file containing Mr James William Durrant’s banking information appears to have been relabelled as “fee notes”, an act that speaks volumes about the priorities and practices of those involved.

Taken together, these records demonstrate that the organisation cannot be relied upon to act in any legitimate trustee capacity. The absence of governance, transparency, and accountability raises serious questions about its continued suitability to operate within the trust services industry. Proper regulatory scrutiny is not only justified, but essential — both to protect the integrity of the industry and to prevent harm that ultimately affects society as a whole.

Set out below is an extract from Anna Kingsland-Jones’s Subject Access Request (SAR), which lists a number of properties and records their ownership over time. These properties correspond to addresses used by Mr James William Durrant during his lifetime and show Anna Kingsland-Jones holding the properties on trust for her father-in-law.

This record further corroborates Anna Kingsland-Jones’s long standing role in relation to Mr Durrant’s property affairs and supports the wider documentary trial demonstrating her trusteeship.

The impostor trustee claims that it has acted as the sole trustee of the Emerald Trust since 23 November 1978. That assertion is untenable for multiple reasons.

Anna Kingsland-Jones and Mr Vaart were the trustees shown for decades and the relevant companies and trust arrangements remained with Barclaytrust in Jersey well into 1979. Only later were management services transferred to the organisation that now styles itself as trustee.

The documentary record makes this clear: the entity now claiming sole trusteeship was, at the relevant time, providing fund management services, not acting as trustee. Its assertion that it has been the sole trustee since November 1978 is therefore irreconcilable with the contemporaneous documents and the established timeline. When that timeline is applied, it follows that the deed purporting to name the Freemasons as beneficiaries is not genuine and could not have validly governed the trust.

The Durante family holds extensive records which, once released, will result in a significant financial disclosure with far-reaching consequences across the industry. When that material becomes public, it is difficult to see how any reasonable person would place trust in the law firms and organisations involved.

The next post will address the fact that the impostor trustee was, in reality, acting as a fund manager. This is readily demonstrated by over one hundred letters, written between 1979 and the late 1980s, in which the fund manager repeatedly wrote to Mr James William Durrant requesting fee notes for management services relating to his companies. This correspondence is further supported by bank statements from the Emerald Trust, which show payments being made to them in their capacity as fund managers, not trustees.

The documentary trail is clear and consistent.

Thank you for reading, and have a good weekend.

Kind regards,

Jordan Durante

Comments