From Fund Manager to Trustee: Power Seized After a Financially Motivated murder.

- jordandurante81

- Dec 22, 2025

- 8 min read

The Emerald Trust Deed Produced After the Murder

Following the murder of Mr James William Durrant, a trust deed was later produced in Jersey[after the original murder inquiry was shut down] purporting to be the Emerald Trust. This document does not contain Mr Durrant’s name, the names of any of his family members, nor Mr Durrant’s signature. On its face, the deed is therefore not associated with Mr Durrant.

Despite this, the document was relied upon to assume control of Mr Durrant’s trust structures and associated companies after his death.

Crucially, this Emerald Trust deed was never presented to the bank that held the Emerald Trust bank account and its related company accounts. When the entity now acting as trustee later communicated with the bank, the bank stated that it had never heard of them and required formal authority by way of a valid trust deed. The bank already held Mr Durrant’s specimen signature on file and required documentary proof consistent with its records.

No such deed was ever provided to the bank.

The bank’s own files confirm that the purported trustee failed to establish authority. The implications of this omission — and access to the bank’s complete records — will be addressed in detail in a forthcoming section and how Mr Smalley and the impostor trustee have kept income and capital separate as they did not know who the true beneficial owners were.

It is also important to note that the individuals behind the entity now acting as trustee were well acquainted with Mr Durrant. Many staff had previously worked at Barclaytrust International, which acted as fund manager for Mr Durrant for a period. Mr Durrant later removed control and management from Barclaytrust International and transferred fund management to this new firm.

At no point were they appointed as trustee during Mr Durrant’s lifetime. Their role was limited to fund management, not trusteeship.

The production of a trust deed after the settlor’s violent death — a deed that lacks his name, his family’s names, and his signature, and which was never accepted by the bank — raises serious and unresolved questions about how control of the trust and companies was assumed.

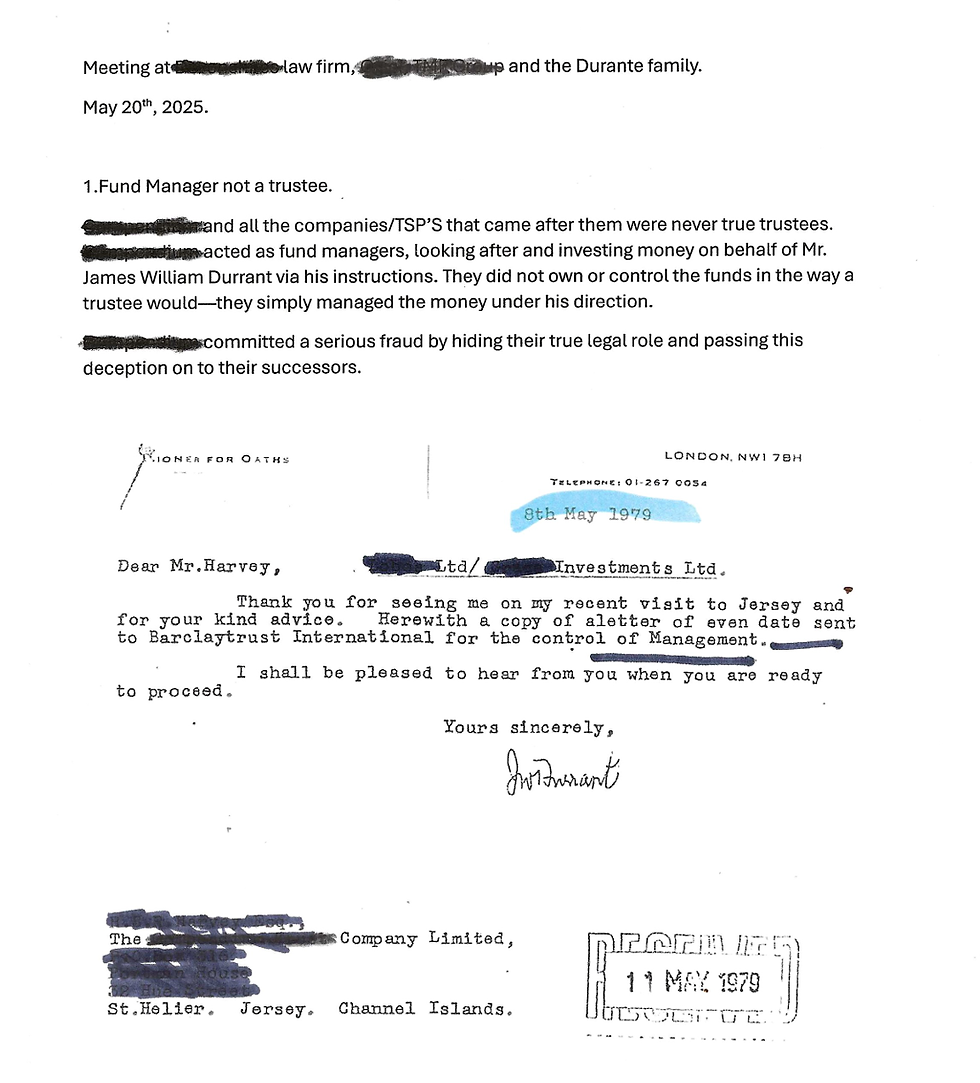

What Mr Durrant’s Letter Reveals

The above letter written by Mr James William Durrant to a prospective new fund manager demonstrates that the trust deed dated 23 November 1978 could not have operated in the manner later claimed.

At the time of the letter, the Emerald Trust and its associated companies remained under the management and control of Barclaytrust International. This is wholly inconsistent with the assertion that a different entity had already become trustee in November 1978.

The letter further confirms that Mr Durrant was in the process of transferring fund management only, not trusteeship. The language used is explicit: management and control were to be passed to a new fund manager, not to a trustee, and certainly not to the entity now asserting that it had assumed sole trusteeship at that time.

Taken together, the contemporaneous documentary record shows that:

Barclaytrust International continued to manage the structures after November 1978;

No trustee change is evidenced or authorised;

The later claim of trusteeship is incompatible with Mr Durrant’s own written instructions.

This contemporaneous correspondence therefore directly contradicts the later narrative and raises serious questions as to how and when trusteeship was allegedly assumed.

Further Evidence of Fund Management — Not Trusteeship

The above letter, dated in the early 1980s, is further correspondence from Mr James William Durrant to his new fund manager. In this letter, Mr Durrant sets out the exact monetary amounts payable as fee notes for the management of his companies.

The significance of this document is straightforward: it evidences a commercial fund-management relationship, not a trusteeship. The fees described relate specifically to the administration and management of companies on Mr Durrant’s behalf, consistent with the role of a fund manager acting under instruction from the owner and settlor.

There is no reference in the letter to:

the appointment of a trustee,

the transfer of trusteeship,

or the relinquishment of control by Mr Durrant.

Instead, the correspondence reinforces the contemporaneous position that the firm was being engaged to manage assets, not to hold them as trustee. This again conflicts with later claims that the same entity had already assumed trusteeship during this period.

When read alongside earlier correspondence and bank records, the letter forms part of a consistent documentary trail showing that trusteeship remained unchanged during Mr Durrant’s lifetime, and that later assertions of trusteeship are not supported by the evidence.

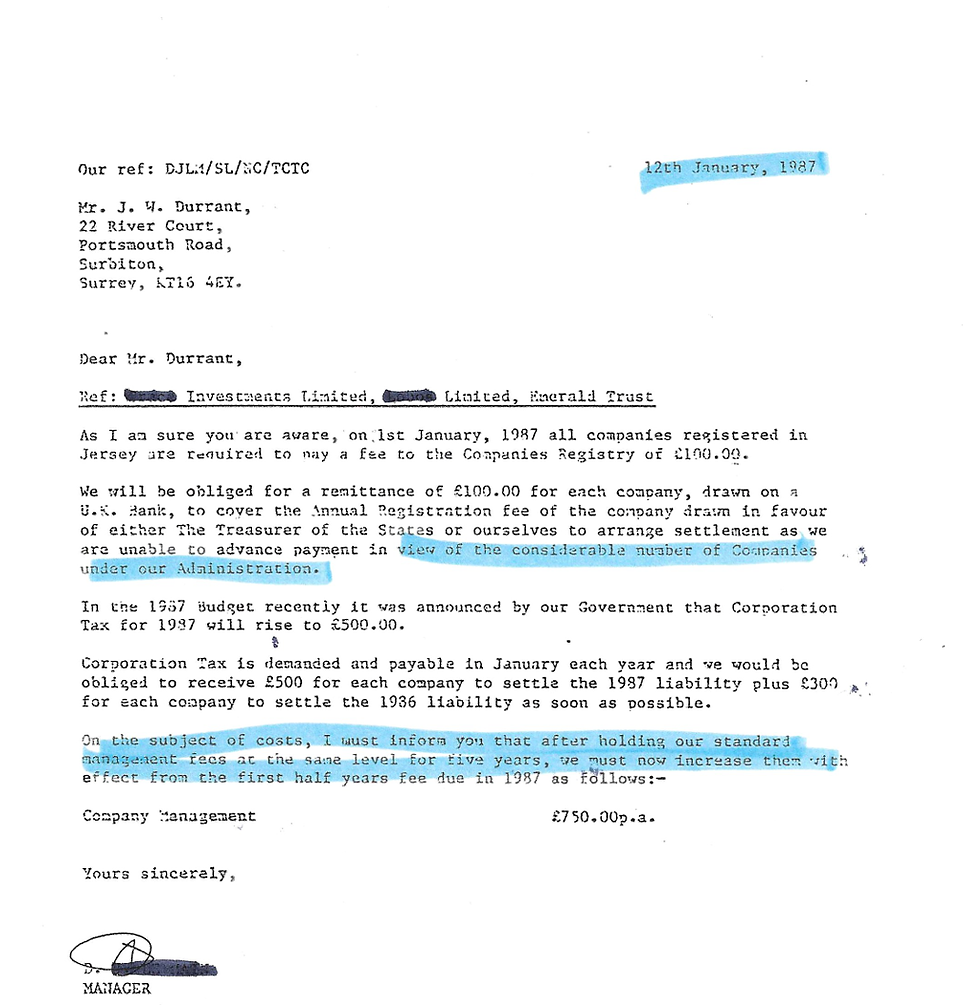

Management Fees Confirm Fund Manager Status

The above letter from Mr Durrant’s fund manager contains a clear reference to standard management fees, noting that those fees had remained unchanged for the previous five years and now required an increase.

This detail is significant. The discussion of fee notes, standard management charges, and periodic fee reviews is characteristic of a fund management relationship, not that of a trustee. Trustees do not typically describe their remuneration in this manner, nor do they frame their role as ongoing “management” subject to standard fee adjustments over time.

The letter therefore provides further contemporaneous confirmation that, while Mr Durrant was alive, the organisation’s role was confined to fund management services. It does not evidence trusteeship, nor does it suggest that control of the trust structures had passed from Mr Durrant.

Taken together with earlier correspondence, this document reinforces a consistent pattern: throughout Mr Durrant’s lifetime, these organisations acted as fund managers, not trustees, and any later claim to trusteeship is not reflected in the contemporaneous records.

Fee Notes Paid From the Emerald Trust Account

The above letter from Mr Durrant’s fund managers sets out the exact amount requested for their fee notes in respect of managing the Durrant companies.

Below this is a letter from Mr James William Durrant to the same fund manager, enclosing a cheque for the precise amount requested: £1,312.54. The payment is explicitly made in settlement of management fees.

Beneath that correspondence is a screenshot of the Emerald Trust bank statement, which records the same payment of £1,312.54 being debited from the Emerald Trust account and paid to the fund manager.

The significance of this sequence is clear and verifiable:

the fund manager invoiced for management services;

Mr Durrant authorised payment of the stated amount;

the payment was made from the Emerald Trust bank account;

the recipient was the fund manager — not a trustee.

This bank account is the very account over which the same organisation later claimed trusteeship following Mr Durrant’s murder. The contemporaneous records therefore show the organisation acting as a paid fund manager, receiving fees authorised by Mr Durrant during his lifetime, not as a trustee exercising control.

The documents form a complete evidential chain: invoice, authorisation, and bank payment — all of which pre-date the later claim to trusteeship.

Payment to the Fund Manager From the Emerald Trust Account

Shown below is the payment made from the Emerald Trust bank account to Mr Durrant’s fund manager. At the time this payment was made, the recipient was acting in the capacity of fund manager, not as trustee.

The payment corresponds precisely with the fee notes issued for management services and was authorised during Mr Durrant’s lifetime. It therefore evidences a commercial management relationship, rather than the exercise of trusteeship.

This same bank account was later relied upon by the fund manager in asserting control after Mr Durrant’s murder, despite the contemporaneous records showing that they were being paid as a service provider, not acting as trustee.

The Bank Mandate That Confirms Trusteeship

Below is a letter from Royal Trust Bank addressed to Christopher Durante. Enclosed with the letter is the original bank mandate for the Emerald Trust account as the bank knew the true beneficial owners of these monies.

For decades, lawyers acting for Mr Smalley and the entity now claiming to be trustee repeatedly stated that no bank mandate could be located and that, as a result, they could not determine the true ownership of the Emerald Trust income and funds. This explanation was used to justify keeping rental income and substantial sums of money “separate” and undistributed.

The recovered bank mandate directly contradicts those claims.

The mandate clearly identifies Mr James William Durrant as trustee, confirming that the fund manager was not the trustee of the Emerald Trust. This contemporaneous banking document resolves the question of authority that was said to be unknowable for decades.

Because the bank recognised Mrs Durrant as the appropriate point of contact, Mr Smalley and the fund manager were required to seek Mrs Durrant’s authorisation to access the Emerald Trust bank account. This is consistent with the bank’s records and inconsistent with the later assertion that the fund manager had already assumed trusteeship and had been since 1978.

Following the execution of a will prepared for Mrs Durrant by Mr Smalley, she suffered a stroke six days later. Thereafter, uncertainty was claimed as to the identity of the true beneficiaries, and income and capital were again retained rather than distributed. However, with the bank mandate now located, that uncertainty no longer exists.

The existence of this mandate means that the withheld funds and accumulated income can now be accounted for and transferred lawfully, in accordance with the trust’s true structure and authority.

It also provides a credible explanation for why the trust’s assets and income appear not to have grown since 1988: contemporaneous evidence suggests that income streams were diverted or withheld following the violent death of the settlor.

The Address and Name Shown on the Bank Mandate

Readers should note that the address recorded on the Emerald Trust bank mandate is Alan Way. When this is compared with the Subject Access Request (SAR) records for Anna Kingsland-Jones, the same property is shown as being held by her as trustee for Mr James William Durrant.

This alignment between the bank mandate and the SAR material is significant, as it places the trust’s banking authority and the property record within the same factual framework.

Readers may also observe that on the right-hand side of the mandate a number of names have been partially redacted with “XXXXXX”. Beneath those redactions, the remaining visible lettering appears consistent with the name “Kingsland”. While redactions prevent absolute confirmation, the positioning and context are notable when viewed alongside the SAR disclosures.

Further documentary evidence will be published showing that Anna Kingsland-Jones personally funded property purchases, including 20 Wild Oaks, using monies transferred from Royal Trust Bank in the name of the Emerald Trust. These transactions are consistent with her acting in a trustee capacity on behalf of Mr Durrant and are incompatible with later claims that a fund manager had assumed trusteeship and that they had been the sole trustee since 1978 !

Together, these records reinforce a consistent picture: the Emerald Trust’s banking authority, property holdings, and funding decisions were aligned with Mr Durrant and his family during his lifetime, not with the entity that later asserted control.

Note: It is also relevant that Robert Maxwell used the same organisation as fund managers during his lifetime, reinforcing the historical role of that entity as a fund manager, not a trustee.

“The name on the right-hand side of the bank mandate has been partially redacted. While the remaining visible lettering appears consistent with the name ‘Kingsland’, the redaction prevents definitive identification. Readers are invited to consider this alongside the SAR disclosures and property records showing Anna Kingsland-Jones acting as trustee for Mr Durrant.”

hj

What Comes Next

A forthcoming post, to be published tomorrow or very shortly, will examine how Mr Smalley and the entity now acting as trustee obtained access to the Emerald Trust bank account, and why trust income and substantial sums of money were kept separate for decades.

That post will set out the documentary trail explaining how control was exercised, how authority was asserted, and why funds were not distributed during that period.

Thank you for reading. If you require assistance, wish to share information, or have experience of corruption or related abuses involving trust structures, you are welcome to make contact via this website.

Kind regards,

Jordan Durante

Comments